The semiconductor industry's explosive growth in AI compute capacity hinges on a single piece of equipment manufactured by one Dutch company. ASML's EUV lithography machines represent the technological frontier for producing the densest, most power-efficient chips that power modern large language models and neural networks. Without these systems, chipmakers like TSMC and Samsung cannot fabricate the sub-5nm process nodes required for next-generation AI accelerators. As demand for AI inference and training capacity continues its steep trajectory, ASML has become the de facto gatekeeper of AI infrastructure expansion—and that gate is narrower than the industry needs it to be.

The production bottleneck is real and consequential. ASML currently manufactures only a handful of EUV systems annually, each costing upward of $150-200 million and requiring months of installation and calibration at customer facilities. The company's decision to significantly increase production output addresses a critical market reality: every major AI infrastructure player—from cloud providers building out data centers to chipmakers racing to secure manufacturing capacity—is competing for limited EUV machine allocation. This supply constraint has become a primary limiting factor in how quickly the industry can scale AI compute, making ASML's production roadmap arguably more strategically important than any individual AI model release.

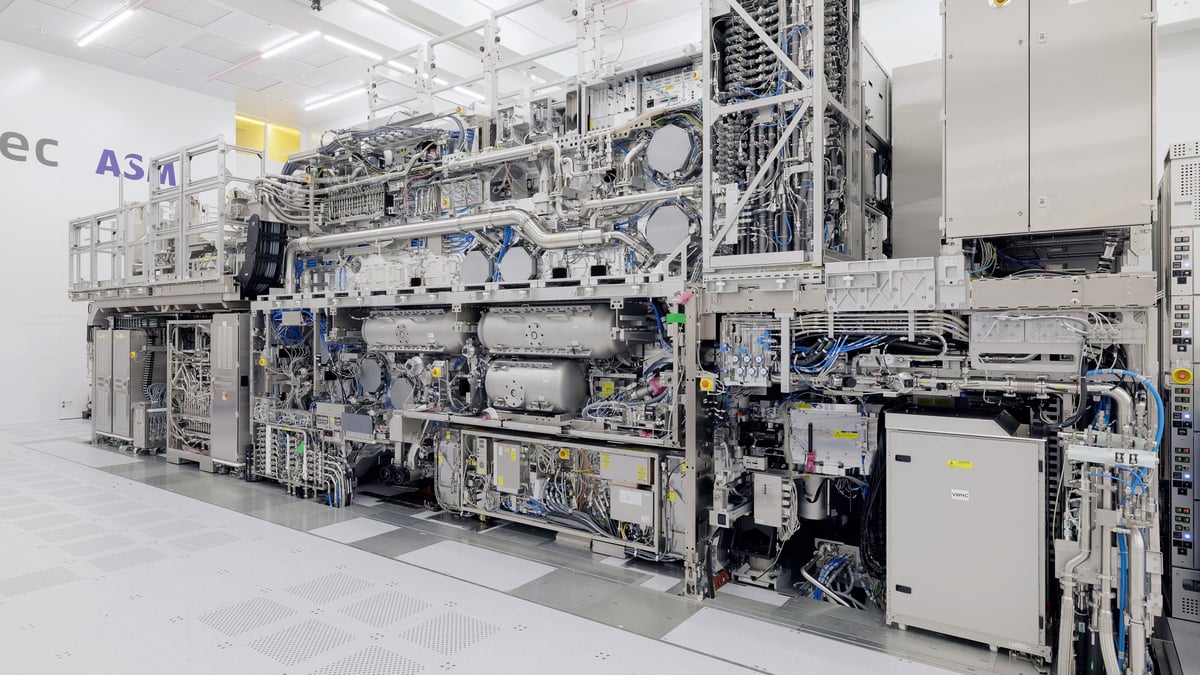

From a technical perspective, ASML's EUV systems operate at 13.5-nanometer wavelengths, enabling feature sizes below 10 nanometers through advanced resolution enhancement techniques and multiple patterning strategies. The machines themselves represent extraordinary feats of precision engineering—they must maintain nanometer-scale accuracy across wafers measuring 300mm in diameter while operating at extreme temperatures and pressures. The complexity of manufacturing these systems means ASML cannot simply scale production linearly; each additional machine requires expanded factory floor space, specialized clean-room infrastructure, and a highly trained workforce capable of assembling and testing components with tolerances measured in picometers. The company's expansion plans involve building new manufacturing facilities and training programs to increase annual output from roughly 30-40 systems per year toward 50+ units—a significant increase that still may not fully satisfy market demand.

This supply constraint exists within a broader geopolitical and economic context that makes ASML's production capacity even more critical. The Dutch government, working with the U.S. and allied nations, has imposed export restrictions on advanced semiconductor manufacturing equipment destined for China, effectively using ASML's monopoly as a strategic tool in technology competition. Simultaneously, major chipmakers have been investing heavily in capacity expansions, with TSMC, Samsung, and Intel all competing for ASML's available machine slots. The result is a market where access to EUV lithography has become a determining factor in which companies can participate in the AI boom and which are left behind.

The architectural implications extend throughout the entire AI compute stack. Chipmakers must design their roadmaps around ASML's production schedule, not the other way around. This means AI infrastructure providers planning data center expansions must forecast their chip needs 18-24 months in advance and secure manufacturing commitments accordingly. Any delay in ASML's production expansion directly translates into delayed chip availability, which cascades into delayed AI service deployments and slower infrastructure scaling across the industry. For developers building applications that depend on specific hardware capabilities, understanding ASML's production trajectory becomes as important as understanding GPU roadmaps.

CuraFeed Take: ASML's production expansion is necessary but insufficient—the company is solving a constraint that will likely remain binding for the foreseeable future. Even with aggressive scaling, ASML will struggle to fully satisfy demand from every major chipmaker simultaneously. This creates a hidden winner: companies with existing strong relationships and long-term supply agreements with ASML (primarily TSMC) gain structural advantages in the AI chip market. For developers and infrastructure builders, this means the constraint isn't primarily technical anymore—it's logistical and geopolitical. The real question isn't whether EUV technology works; it's who gets access to the machines. Watch for secondary effects: increased investment in alternative lithography approaches (high-NA EUV, next-generation extreme UV), potential antitrust scrutiny of ASML's market position, and accelerated geographic diversification of chip manufacturing capacity outside ASML's export-restricted markets. The company racing to build more machines is actually racing to maintain its monopoly in a world where that monopoly has become too powerful to ignore.